Wildcats Stayed a Century, Will Multiple Issuer Stablecoins Do the Same?

Under every great monetary experiment lies the same question: who do you trust when everyone’s printing money?

When they say kill your darlings, President Andrew Jackson took it literally. In 1837, he dismantled America’s central banking infrastructure by shutting down the Second Bank of the United States.

With the pillar of national finance gone, a wave of loosely regulated banks exploded across the country with many located in such remote areas that people joked they were “where wildcats roamed.” This chaotic period, known as the wildcat banking era, triggered nearly a century of monetary confusion and fragility.

Welcome to the Sovereign Desk.

The consequences were brutal. States and private institutions issued their own currencies, resulting in more than 1600 different banknotes, each valued differently depending on geography and the issuing bank’s credibility. Some of the notorious currencies during the wildcat era:

- Detroit Bank (Michigan) - $2 notes from early 1830s, part of Michigan’s wildcat explosion under the 1837 Free Banking Act.

- Farmers’ Exchange Bank (Rhode Island) - Early 1800s bank issuing notes in remote Connecticut/Rhode Island wilderness before formal state charters, one of the very first true wildcat banks.

- Kirtland Safety Society (Ohio) - A quasi-bank founded by followers of Joseph Smith in 1837; printed notes without charter and swiftly collapsed.

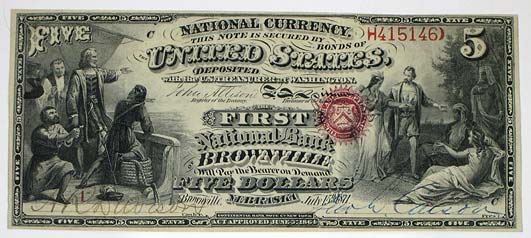

- National Bank of Brownville (Nebraska) - $5 issued under a territorial charter with minimal oversight

Imagine someone today discovering their IKEA gift card is actually worth half once they cross into another state…and realizing they now need a conversion table just to buy a lamp.

If you were a traveling cowboy, you lost money almost every time you moved between states. Exchanging notes could cost you roughly 30% to 60% in total. Merchants had to consult a guidebook to sort real from fake bills.

For central banks, this raises an old problem with a new face: What happens when too many players issue dollars without direct accountability?

Just as wildcat banks once butchered the integrity of currency, multiple-issuer stablecoin ecosystems could introduce modernly dressed familiar problems especially in emerging markets where dollar-pegged assets fulfill what local currency cannot. Not to mention tech giants exploring the same avenue, possibly introducing their own stablecoin currency down the line.

However, not all wildcat banks were predatory, and not all stablecoin issuers are reckless. This is where the regulatory bodies should procure preventive measures. The wildcat system failed not because of bad actors alone, but because it lacked regional coordination, oversight, and support during stress. The Fed solved those by centralising just enough power while maintaining regional and private-sector participation. But what about the decentralisation pillar as part of the classic blockchain trilemma?

Today’s stablecoin landscape, by contrast, is hyper-global and ruthlessly efficient - compared to the 1800s where logistics are physical with banks' power local, but fragile. These days liquidity doesn’t even sleep. But how long can this momentum last?

Tension and pressure builds as the adoption scales across all fronts - retail and institutional begins to incorporate stablecoins like they do with AI in 2021. The future of multiple issuer stablecoins, particularly in emerging markets, seems to narrow toward several defining scenarios.

Coordination vs Fragmentation

Scenario A: US leadership with the GENIUS Act

If the GENIUS Act passes as drafted, large stablecoin issuers would fall under federal oversight (OCC for >$10 B coins; state for smaller) with enforced 1:1 reserves in liquid assets and monthly audits. This could create clarity for top-tier issuers like Circle, while pushing opaque ones like Tether offshore. A US-centered hub would emerge, reducing regulatory arbitrage and potentially centralising liquidity around compliant issuers.

Scenario B: Regulatory arbitrage and offshore flight

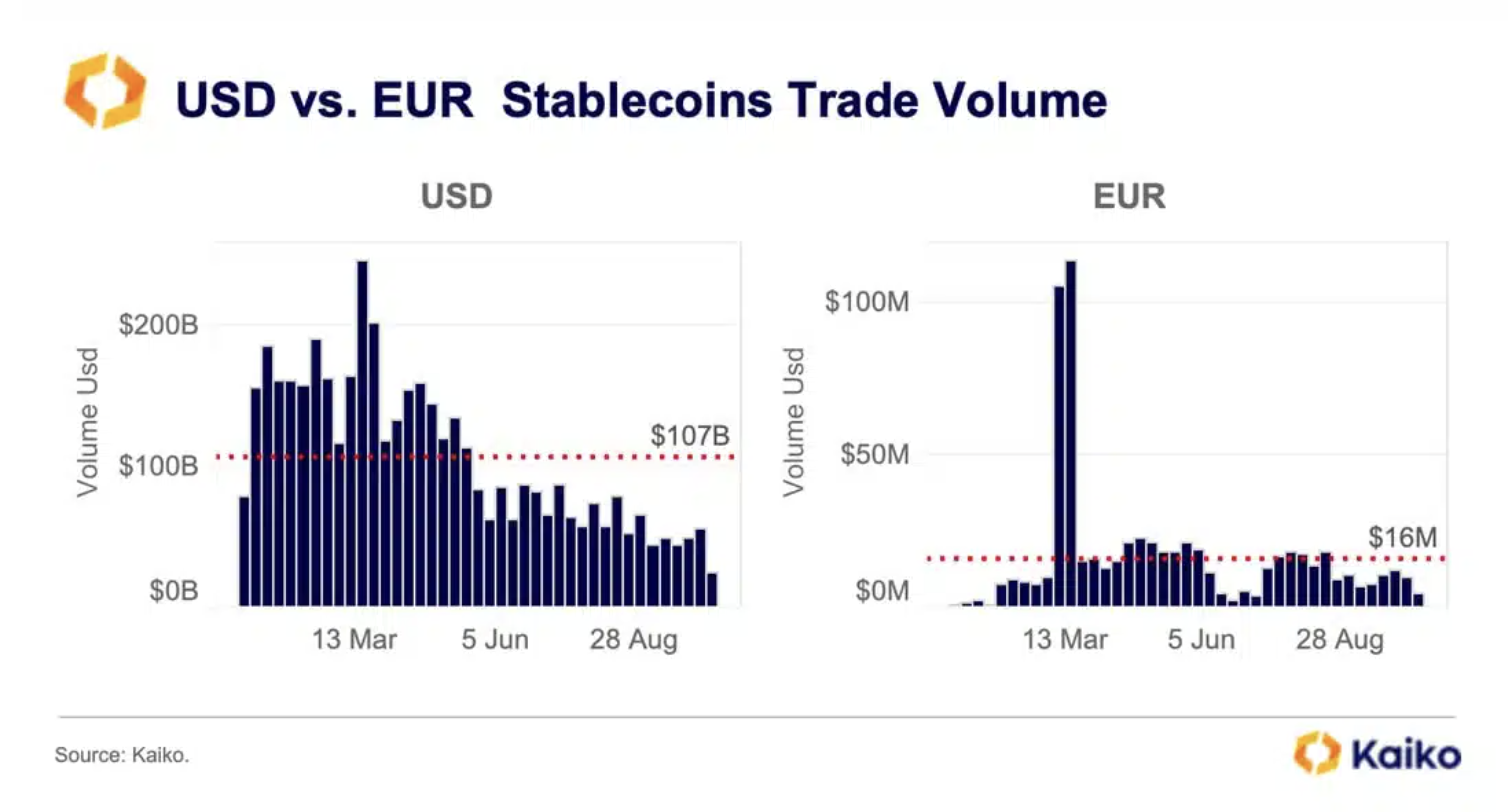

Source: Kaiko

If US regulation stays fragmented, or carves out large non-US issuers, stablecoin issuers will gravitate to crypto-friendly jurisdictions like El Salvador or SPDI-specialized states such as Wyoming. This could lead to fragmented trust networks, with stablecoins circulating in isolated “zones,” and in turn increasing shadow liquidity and systemic risk.

Central Banks Joining the Game

Scenario A: ECB and digital euro accelerates

The ECB is pressing for digital euro legislation, explicitly motivated by concerns over privately issued stablecoins encroaching on monetary sovereignty. If China and others follow, we could see a multi-currency digital ecosystem where private multi-issuer stablecoins coexist - under the watchful eye of central banks. However, the real tension is this: who settles in digital euros… when the world already runs on digital dollars?

Scenario B: Global fragmentation continues

Without coordinated rules, stablecoin rules will vary widely (EU under MiCA, US under GENIUS, others under light frameworks), leading to an ecosystem fractured by compliance barriers. Cross-border stablecoin use may thrive among institutions, but face limited consumer adoption.

Institutional vs. Retail

Scenario A: Bank-issued stablecoins grow

If banks integrate stablecoins as deposit substitutes, systems evolve toward regulated, backed tokens. BIS and S&P suggest aligning stablecoin risk with bank regulation (“same activity, same risk, same regulatory outcome”). These bank-backed coins might hold the twin strengths of decentralisation’s tech and centralisation’s trust.

Scenario B: Fintech and ledger-native usage

If big tech (Amazon, Stripe, Mastercard) and DeFi protocols (Curve, Uniswap, decentralized L1s) lean on privately issued stablecoins, adoption could flourish but likely in a segmented, tech-driven ecosystem where liquidity pools and shadow chains thrive alongside (but not within) the traditional banking systems.

Systemic Risk and Spillovers

Multiple issuer stablecoins mean shared exposure to US Treasuries and liquidity pools. Moody’s warns a stablecoin crisis could depress Treasury prices - or generally impacting monetary sovereignty and financial stability. A major depeg or large-scale issuance could ripple into traditional banking, and necessitate a coordinated supervisory response.

The Role of Fragmentation in DeFi

DeFi is already embracing plurality in stablecoins, e.g., USDT, USDC, DAI, PYUSD, USDG. Amberdata reports rising issuance and velocity across stablecoins, with ecosystem diversification. Yet, fragmented issuance risks fragmented liquidity, requiring cross-chain bridges and AMM mechanisms that add complexity and vulnerability to arbitrage and flash crashes.

The wildcat era was born from decentralization without coordination, collapsing under the weight of its own fragmentation.

Today’s stablecoin ecosystem enjoys greater speed, deeper liquidity, and programmable resilience. However it has already experienced cracks in the form of depegs. Even “safe” stablecoins like USDC have temporarily lost their peg under stress (e.g., March 2023 during SVB collapse). Furthermore it faces the same core dilemma: how do you scale trust across borders, chains, and issuers without igniting chaos?

Ironically, rising interest rates could benefit centralized issuers like Tether. They boost yield on U.S. Treasuries and fatten reserve income; something Arthur Hayes has flagged as a hidden profit engine here. Simply put, the company is becoming a shadow money market fund - without the same regulatory guardrails.

And then there’s UST. Their infamous collapse in May 2022. Without collateral, they rely solely on theory-fed incentives, which unravel fast in crises, where theory is tested in practice. Unlike USDT or USDC, UST tried to maintain their peg via smart contract logic, not reserves. The collapse of Terra-Luna in 2022 vaporized $40B.

Our financial future doesn’t demand a carbon copy of the Federal Reserve. But it will demand something, some form of equilibrium between innovation and order. The pressure to standardise will mount as adoption spreads.

Until then, stablecoins walk a narrow ridge between efficiency and fragility. Like the cowboys of 1837, users now ride fast across the frontier but they still carry shenanigans in their saddlebags. When trust fades, even the smartest contracts turn into paper ghosts.

The Sovereign Desk editorial is open for conversation. If you’ve observed notable flows, rumours, or data points that warrant attention, please reach out to us:

Dendi Suhubdy at [email protected]

Faisal Mujaddid at [email protected]

Looking to execute large crypto trades with precision, privacy, and zero slippage? Schedule a call with the team at t.me/dendisuhubdy or shoot us an email at [email protected]. Bitwyre’s OTC desk handles high-volume transactions with deep liquidity and bespoke settlement.

We’re also rolling out a stablecoin payments app that lets you bypass OTC entirely, allowing you to use your stablecoins directly for payments at Visa-supported merchants worldwide. Sign up for the waitlist here.