Who’s Afraid of the Commodity Label?

The Congress banters over what crypto really is

If your token falls under the definition of a security, it enters the SEC’s domain, bringing with it obligations around disclosures, audits, and the ongoing regulatory scrutiny. If it qualifies as a commodity, the oversight generally shifts to the CFTC, which tends to focus on derivatives and takes a lighter touch on spot markets. It’s understandable, then, why many protocols post-FTX have sought the relative clarity and simplicity of the “commodity” label.

But in crypto, definitions are rarely straightforward, and the real risk often lies in how those lines are drawn, and who ends up redrawing them.

Welcome to the Sovereign Desk.

The battle for crypto’s legal identity is now happening in Congress, where a single word could change everything. Commodity. Say it in the wrong corridor on Capitol Hill and you might trigger a call from legal followed by a calendar ping for “follow-up after markup.” In crypto’s bloodsport of money, power, and interpretation, no designation is more cryptic, more coveted, or more contested.

The GENIUS Act, formally Giving Expanded National Investment Understanding and Safeguards, promises to draw a bold line between decentralised tokens and securities, pushing those assets toward CFTC jurisdiction. The CLARITY Act, on the other hand, endeavours to define how a token can mature from a startup fundraising device to a network utility or store of value. At first glance, both bills seem like wins for the industry. But you’re not here to read the obvious, so we dig deeper into the different game being played: one with serious consequences.

The Act clearly has its champions, but not everyone is convinced it’s a stroke of brilliance. Some critics argue that while it lays groundwork for stables’ expansion, it sidesteps some of the messier national security concerns: without robust anti-money laundering protections and clear enforcement rules, dollar-backed tokens could become the preferred rails for shadow finance (and the other likes).

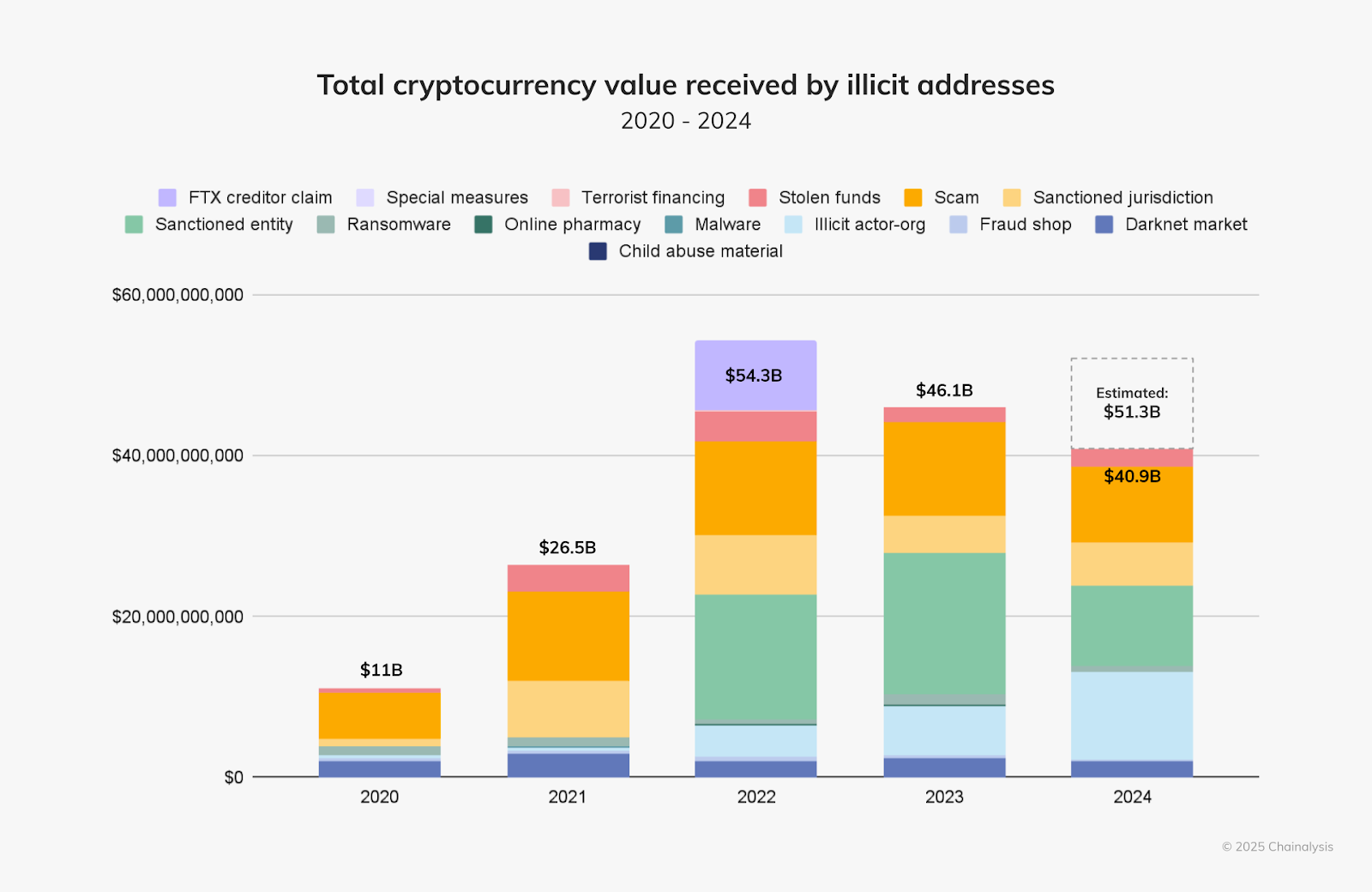

The numbers aren’t theoretical either, illicit crypto flows have surged past $50 billion annually, with stablecoins increasingly woven into scam networks, sanctioned jurisdictions, and stolen funds. GENIUS punts many of these issues to “further study,” which some read as code for “let someone else deal with it.”

Founders of major tokens are watching nervously. Many launched their assets with traditional venture models, with the promise for growth and a long roadmap milestones. That’s textbook security behaviour under the Howey test. The CLARITY Act offers a theoretical path to redemption, introducing a four-year safe harbor for primary token offerings, allowing tokens to transition from securities to commodities if the underlying network achieves “mature” status and the total raise remains below $75 million in any 12-month period. However, the criteria are quite opaque, without a clear timeline in sight, and the risk of retroactive enforcement lingers. Stablecoin issuers, too, are in limbo. If something pegged to the dollar is treated as a commodity, who regulates the peg? The reserves? The cash flows? GENIUS defers the hard part to “further study,” which might be code for “someone else’s problem.”

Institutional desks aren’t thrilled about this either. These are firms built on risk models, and compliance - they need to know exactly what rules govern their trades, especially when dealing with digital assets that could swing between being treated as securities or commodities. But the lack of a clearly defined jurisdiction between the SEC and CFTC leaves them in limbo. That uncertainty pushes insurance premiums higher, since underwriters price in the legal risk of enforcement or misclassification. It also slows down capital deployment, as desks are reluctant to allocate meaningful size without clarity on how the assets will be treated under federal law. Many hoped the GENIUS and CLARITY Acts would clean up the map, but instead they seem to redraw new lines of conflict, leaving many institutional investors in a state of uncertainty - one that is evident in the cautious approach to investments in Bitcoin ETFs, with institutions holding less than 30% of total assets.

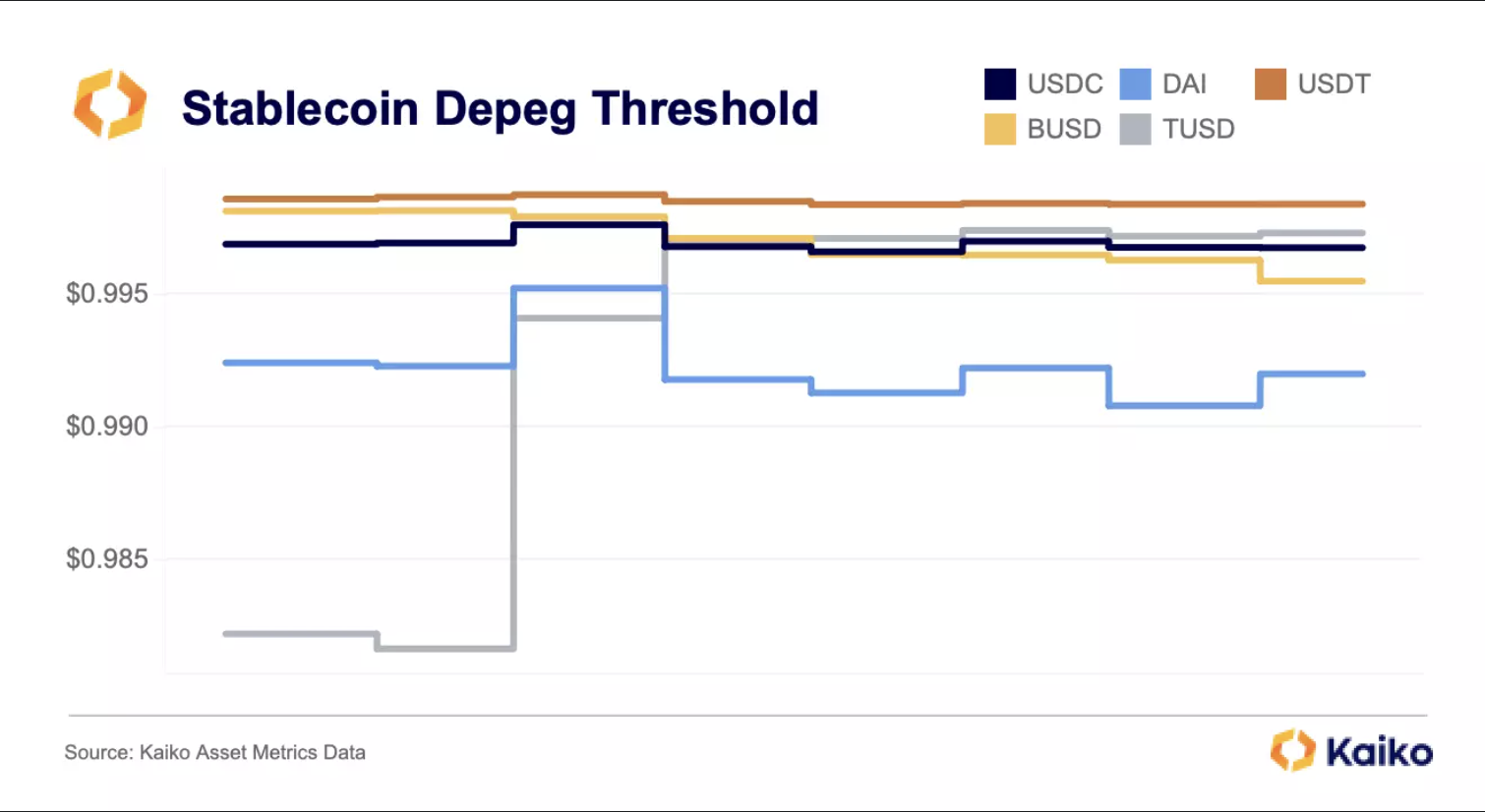

The deeper irony is that the commodity label may not be the blessing it seems. For many tokens, commodities are loosely regulated - yes, but they’re also literally, the wild west. No quarterly filings - unlike securities, commodities are not required to provide regular disclosures, leaving investors with less information about the asset’s performance and risks - No investor protections. No backstop when the market turns. In good times, it feels like freedom. In bad ones, it feels like free fall. If a stablecoin depegs, and no regulator owns the asset class, who picks up the pieces?

There’s also a geopolitical angle that rarely gets mentioned. If the US fast-tracks a CFTC-lite regime, Europe and Asia won’t sit still. Singapore is already tailoring bespoke regulatory channels. Switzerland, through its financial regulator FINMA, has adopted a nuanced approach to stablecoin regulation. France intended to build the next euro-backed infrastructure. With every move, the GENIUS Act risks triggering a new kind of arbitrage, where legal clarity itself becomes the heat, and the jurisdiction with the softest grip ends up with the most value.

And then there’s the commodity curse. Gold, oil, and wheat are some of the classic benchmarks. They’re volatile and politicised. They factor on weather, war, and OPEC tables. Crypto joining that club, means it inherits the same current.

The commodity label carries a certain seduction: fewer disclosures, looser oversight, and the aura of institutional legitimacy. But beneath that surface lies a more urgent question. Who intervenes when systems fracture and no regulator is assigned to catch the fall? In commodities law, there are no prospectus requirements, no circuit breakers, and no disclosure rules designed to protect retail users. Once an asset is classified as a commodity, user safeguards often become a market responsibility or simply fall away.

The CLARITY Act attempts to map a path to legal maturity, where a token might evolve beyond securities law into something more neutral. But the thresholds it proposes for decentralisation to liquidity benchmarks (and the independence of protocols), while remaining vague enough to be interpreted generously and early enough to raise concerns about timing. The GENIUS Act, meanwhile, emphasises innovation and regulatory restraint but says little to the user whose income or savings may be tied up in a token that sits outside a defined supervisory perimeter.

So who is afraid of the commodity label? Not the lawyers and legal persons. Not even the issuers with their clean exits. But perhaps the millions holding assets they believe to be stable, neutral, and unbreakable. Until they are not.

The Sovereign Desk editorial is open for conversation. If you’ve observed notable flows, rumours, or data points that warrant attention, please reach out to us:

Dendi Suhubdy at [email protected]

Faisal Mujaddid at [email protected]

Looking to execute large crypto trades with precision, privacy, and zero slippage? Schedule a call with the team at t.me/dendisuhubdy or shoot us an email at [email protected]. Bitwyre’s OTC desk handles high-volume transactions with deep liquidity and bespoke settlement.

We’re also rolling out a stablecoin payments app that lets you bypass OTC entirely, allowing you to use your stablecoins directly for payments at Visa-supported merchants worldwide. Sign up for the waitlist here.