Going Full Circle: On Top of The Coinbase

The IPO was loud. But Circle’s real challenge is quieter: turning held dollars into moving ones before the yield clock runs out.

Circle went public not long ago and the market loved it. From a modest $31 IPO price, the stock burst through about $87 in hours, triggering ETF filings and earning a “next Visa” whisper campaign from crypto bulls. The hype was thick.

But let's set aside the ticker glow and the congratulatory posts from LinkedIn bros - you’ll see a bit of a void in Circle's future; It is not exactly a payments company as of yet. It’s a $1 billion Treasury fund in a stablecoin costume. Let's strip it naked.

Welcome to the Sovereign Desk.

Yes, exactly. That’s their business model. As of 2024, 99% of Circle’s revenue came from interest, specifically, the yield generated by the quiet $60 billion behind USDC. When people hold the token, Circle earns. When people move it, margins shrink. That there is sort of where the paradox lies.

Generally in fintech, usage is the endgame. But when we look at Circle, it seems that usage is in fact, the cost center.

In most fintech plays, usage is the endgame. But with Circle, usage actually shrinks their profit margin, that is because when people move USDC off-platform or spend it, Circle loses that reserve-based yield. Much of Circle’s distribution comes through Coinbase, which in 2024 collected 60% of gross reserve income (approximately $908 million), according to Circle’s S‑1 filing. In short, every transaction routed via Coinbase chips away at Circle’s bottom line, and that dynamic is baked into their financials.

But let’s be clear: the reserve base is no joke. USDC is a top-tier stablecoin and by no means irrelevant, to the contrary, Circle’s transparency and regulatory alignment even made it a favorite among institutions. But almost a billion dollars of that yield is paid out to distribution partners like Coinbase. So as you can imagine, revenue is up, but net income remains rather underwhelming (almost flat or even negative). Coinbase took $908 million last year alone. Quite the tax on Circle’s success.

And it gets worse. Because Circle’s entire house is built on short-term interest rates. That’s great during a Fed tightening cycle. But what happens when the pivot comes? Analysts estimate that a 25 basis point rate cut could practically shave off $100 million in EBITDA. Now even your barber would argue that ain't a taper. And let’s not get into the details - what if, the interest rate hikes? We might not like that, but Circle may savor the deal. Since almost all of its revenue comes from parking user funds in short-term Treasuries, a Fed hike is in fact, profit. The higher the rate, the fatter the yield on idle USDC. As long as users keep holding and not spending, Circle can sit back and collect. Ironic? More to come?

Which brings us to the existential moment. We're not unfamiliar with projects that once led the narrative often fell when the tables turned. In 2017, the ICO boom (remember the projects with no working products?) collapsed when reality hit, wiping out nearly $700 billion in market cap in just months. Circle’s earnings are tied entirely to macro policy it can’t control. When the pivot comes, revenue could vanish overnight.

So what's Circle's second act?

To survive rate compression, it must flip the model: turn usage from a cost into a business. That means building infrastructure: Stripe-style APIs for subscriptions and payroll, SDKs for wallets and fintechs, off-ramp corridors in Africa and LatAm. It means positioning USDC as a programmable value, evolving from just a Treasury proxy.

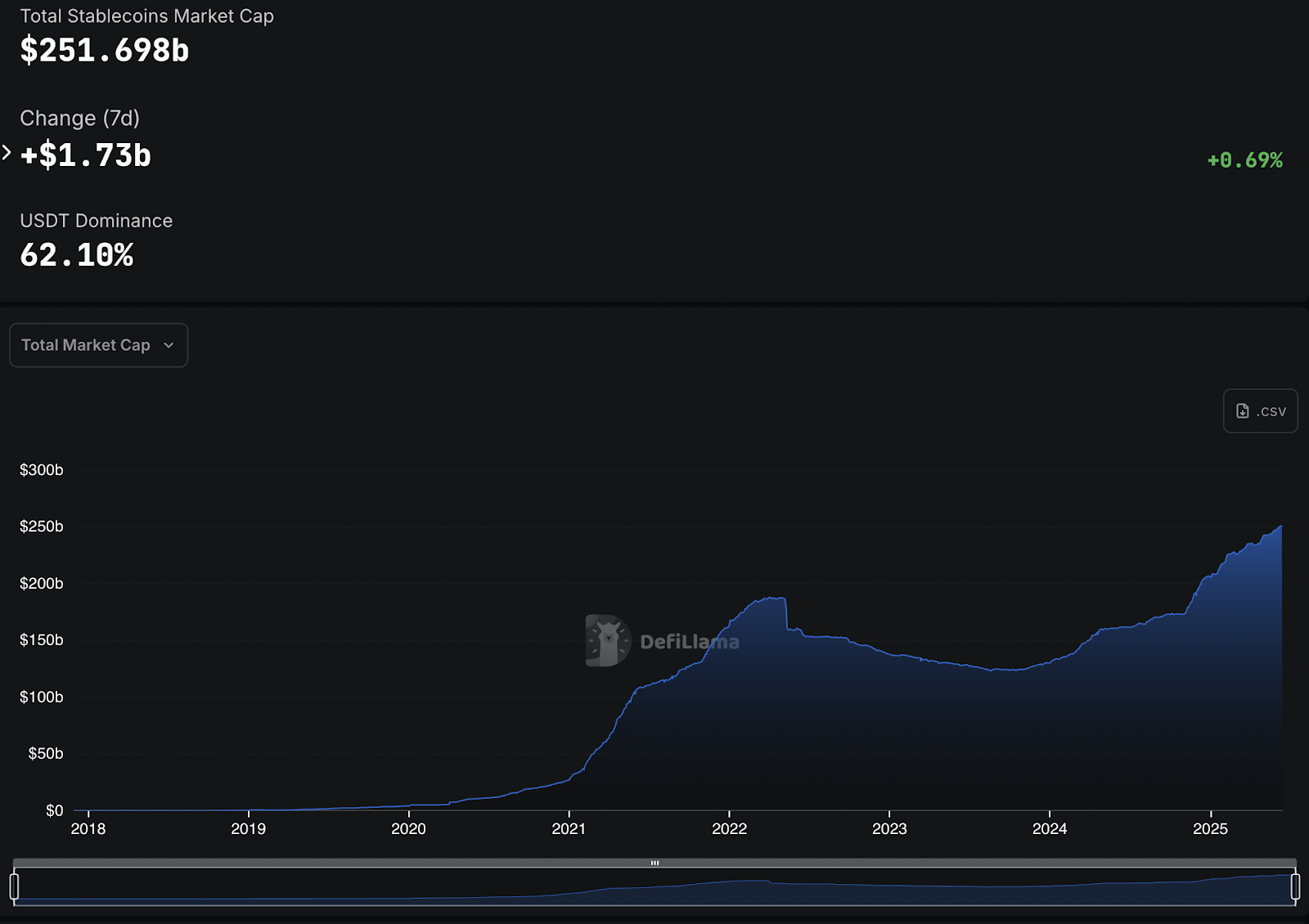

It also means eating the margin pain in the short term to secure dominance in remittances, B2B payments, and digital dollar infrastructure. Because the likely truth is: the first company to solve stablecoin utility at scale will define how money moves globally. But there’s a gap to close. Tether’s USDT still dominates, with a market cap around $155 billion, that's roughly 2.5 times the size of Circle’s USDC at $61 billion. Meanwhile, USDC has nearly tripled from ~$20 billion in early 2022 to today’s levels, a sign of momentum, yes, but it’s still trying to catch up.

What Circle needs to do is to absorb today’s cost drag to narrow that gap. If USDC can’t transform into a medium of exchange, treasury tool, or payments engine, Circle risks remaining the second fiddle in a game defined by scale and flow.

There’s a bigger prize here than just yield farming with U.S. debt. Circle is sitting on the architecture for composable finance. It could be the base layer for digital dollars. The connective tissue between DAOs, fintechs, and sovereign wallets. But it has to evolve, force it if it must. Consider these:

- On curve.finance, USDC plays a leading role in stablecoin swap pools. The USDC/USDT pool, known as Curve’s USD Strategic Reserve, seeing nearly 50x more trading volume than its TVL (about $235 million in trading volume against just $4.7 million locked).

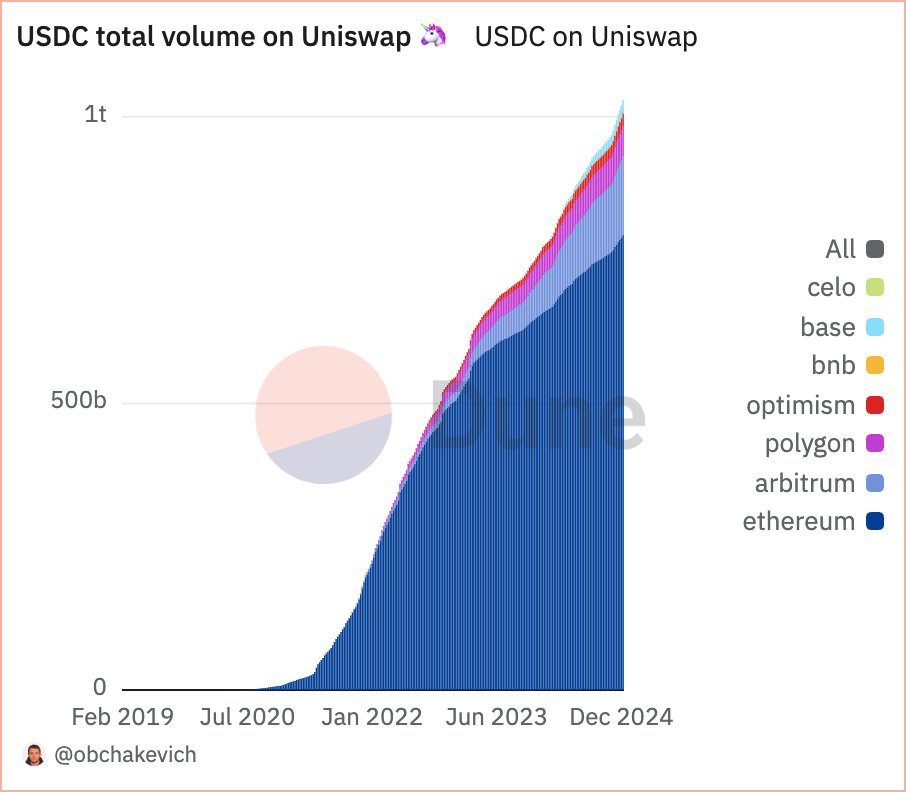

- On Uniswap, as quoted from crypto data analyst @obchakevich_ USDC trading has surpassed $1 trillion in cumulative volume.

These pools see USDC being actively swapped, lent, bridged, and composited into decentralised applications. That’s a quick look at true stablecoin utility. Circle has the capital and the compliance credentials to build powerful rails here.

But in order to fully capitalise, Circle must invest in governance, SDKs, cross-chain tools, regulatory-grade onramps, and merchant integrations. Without those, USDC lacks its own narrative.

So ask yourself, that is if you're part of the craze: “am I buying the future?”. Because the argument here is that you're not really buying a revenue engine at $87, you’re buying the option that Circle becomes the trust layer for 21st century value transfer. If they get it right, it could shift from a treasury proxy to the next Visa - the penultimate rewire, programmable, borderless capital. Or better yet, maybe they should acquire Circle after all. Visa’s last two years have seen it acquire infrastructure players like Pismo, CurrencyCloud, and Tink. With a prior USDC integration (2020) already in the books, an acquisition is the complete package.

If Circle misses the pivot, they’ll be remembered as the most successful money market fund IPO in crypto history.

Either way, the window is now. And the yield clock is ticking.

P.S Jeremy Allaire call us.

The Sovereign Desk editorial is open for conversation. If you’ve observed notable flows, rumours, or data points that warrant attention, please reach out to us:

Dendi Suhubdy at [email protected]

Faisal Mujaddid at [email protected]

Looking to execute large crypto trades with precision, privacy, and zero slippage? Schedule a call with the team at t.me/dendisuhubdy or shoot us an email at [email protected]. Bitwyre’s OTC desk handles high-volume transactions with deep liquidity and bespoke settlement.

We’re also rolling out a stablecoin payments app that lets you bypass OTC entirely, allowing you to use your stablecoins directly for payments at Visa-supported merchants worldwide. Sign up for the waitlist here.